–Overview of the Chloride Process TiO₂ Industry–

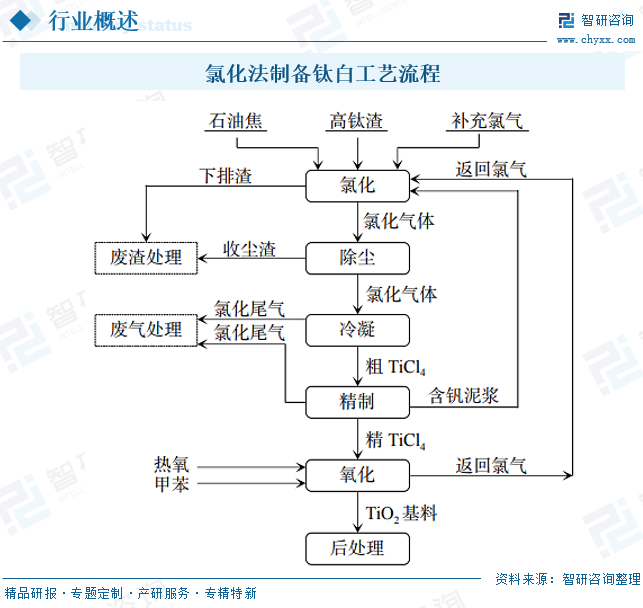

Chloride process TiO₂ is a titanium dioxide (TiO₂) pigment produced through the chloride process. The production process starts with titanium concentrate or high-titanium slag as raw materials, which are chlorinated to form titanium tetrachloride (TiCl₄), followed by oxidation and post-treatment steps to produce the final product. The tio2 chloride process, compared to the sulfate process, offers advantages such as lower emissions, higher product quality (including higher purity, better whiteness, and uniform particle size), and continuous production. It is particularly suitable for high-end applications such as coatings, automotive paints, and plastics.

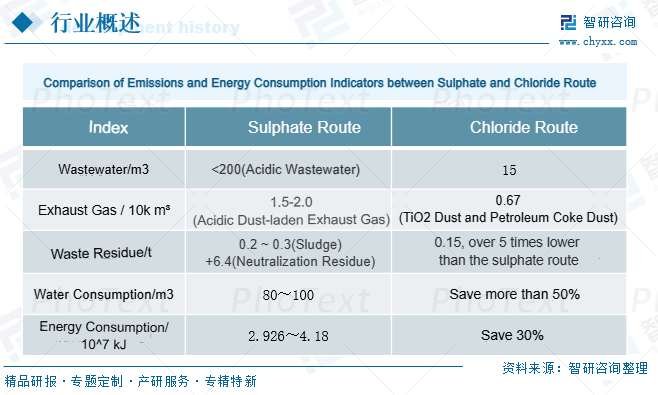

Compared to the sulfate process, the chloride process offers significant advantages in reducing pollutant emissions and energy consumption, making it more aligned with the current requirements for green manufacturing development.

[pwprotect password=”ctio2ch” id=”section1″]

1. Development Opportunities

(1) Policy Support and Environmental Protection Driving Force

The development of China’s chloride-process titanium dioxide industry is strongly driven by policies. The government has included the sulfuric acid process in the “Industrial Structure Adjustment Guidance Catalog (2024 Edition)” as a restricted category, strictly limiting the construction of new sulfuric acid process capacities while encouraging the development of chloride technology. Additionally, the “dual carbon” goals are accelerating the industry’s green transformation. Chloride process, due to its lower carbon emissions (1.8 tons of CO₂ per ton, much lower than sulfuric acid process), has become the focus of policy support, with some local governments offering tax incentives and special subsidies to support enterprises’ technological upgrades.

(2) Market Demand Upgrade and Trend Towards High-end Products

Traditional building coatings demand has been affected by the downturn in the real estate sector, but demand in high-end fields such as new energy (photovoltaics, lithium batteries), automotive coatings, and 5G base station corrosion protection is rapidly growing. For instance, the demand for titanium dioxide in photovoltaic backsheets grows by 27% annually, and each 1GWh of electric vehicle batteries requires 15 tons of titanium dioxide. Chloride process products outperform sulfuric acid process in terms of weather resistance and whiteness, driving substitution in the high-end market. It is expected that by 2030, high-end chloride products will account for 65% of the market.

(3) Technological Advances and Domestic Breakthroughs

Domestic enterprises, such as Longbai Group and Panzhihua Steel, have overcome key technologies like fluidized bed chloride and molten salt chloride. The cost of domestic catalysts has been reduced by 40%, and single-line capacity has increased to 150,000 tons per year. Panzhihua’s 60,000-ton chloride production line has achieved a 99.8% high-quality rate, breaking the foreign monopoly and filling the gap in the domestic high-end titanium dioxide market. Additionally, the successful development of electronic-grade high-purity titanium dioxide (purity ≥99.999%) provides support for emerging fields such as semiconductors.

2. Challenges

(1) Limited Access to Technology

Mature and reliable chloride-process titanium dioxide technology remains a core bottleneck for the development of the domestic industry. Although domestic companies have accumulated some experience through the operation of fluidized bed chloride equipment, those planning to build large-scale chloride production lines still face difficulties in acquiring technology. Currently, advanced chloride-process technologies are mainly controlled by international giants such as Chemours and Tronox, and domestic companies need to break the blockade through independent R&D or technological cooperation. Therefore, obtaining stable and efficient chloride-process technology remains the primary task for domestic industry upgrading.

(2) Raw Material Compatibility and Environmental Protection Challenges

China’s titanium ore resources are mainly of the high-calcium magnesium type, while chloride-process technology requires raw material purity to be high, thus relying on imported low-calcium magnesium titanium ore or processed high-titanium slag, leading to dependence on the international market for raw material supply. Moreover, although chloride process emissions are lower than the sulfuric acid process, its treatment of chlorinated wastewater and waste slag is more challenging, and improper disposal may cause secondary pollution. In particular, the recycling technology for chloride waste slag is not yet fully mature, and the environmental compliance costs are high, posing a significant challenge to the sustainable operation of new projects.

(3) Process Complexity and Technology Route Selection

Chloride-process technology includes two main routes: fluidized bed chloride and molten salt chloride. The fluidized bed chloride process better suits the current demand for large-scale capacity, but its reaction control and equipment corrosion resistance pose high technical barriers. Although molten salt chloride has been industrialized domestically (e.g., Panzhihua Steel), large-scale applications of fluidized bed chloride are still in the research phase. Additionally, the production process involves high-temperature chlorination, oxidation, and other complex reactions, requiring much more precise control of process parameters (e.g., temperature, pressure, airflow speed) than the sulfuric acid process. Any mistake in the process could lead to system failure or substandard product quality.

(4) High Investment Threshold

The investment required for chloride-process production lines is significantly higher than for sulfuric acid processes, with the investment per ton of capacity being 2-3 times higher. For example, a 100,000-ton per year project requires an investment of approximately 2 to 3 billion RMB, and additional environmental protection facilities such as waste heat recovery and exhaust gas treatment further increase the cost. Moreover, the long technology R&D cycle and large risks associated with pilot runs mean that companies need to have strong financial capabilities and risk resistance, creating high entry barriers for small and medium-sized titanium dioxide enterprises.

(5) Reliance on Talent and Experience

Chloride-process production heavily relies on automation control systems, with precise regulation required from raw material chlorination to product coating. The technical team needs to be highly specialized and experienced. Domestically, there is a shortage of engineers with experience in operating large chloride-process plants, and some companies have seen low capacity utilization due to improper operations (e.g., early projects had startup rates below 60%). Furthermore, optimizing core process parameters requires long-term practice and accumulation, and new entrants often face the dilemma of “easy to start, hard to reach full capacity,” which further highlights the strategic importance of talent reserves.

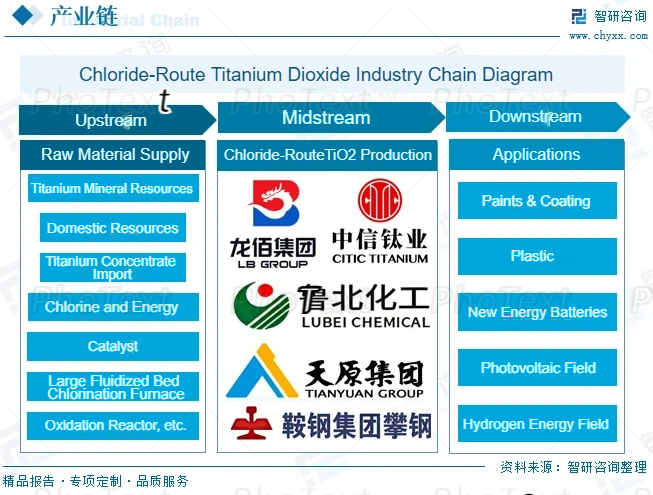

The chloride-process titanium dioxide industry chain in China shows a complete upstream and downstream collaborative development pattern: the upstream is centered on titanium ore resources, with domestic companies breaking through high-calcium magnesium ore limitations through overseas acquisitions and technological innovations (such as molten salt chloride), but low-calcium magnesium titanium ore is still dependent on imports. In the midstream production sector, leading companies like Longbai Group and Panzhihua Steel have mastered key technologies like fluidized bed chloride and molten salt chloride, driving rapid capacity expansion, and it is expected that by 2025, chloride-process products will account for 20% of the market share. The downstream application field is extending from traditional coatings and plastics to high-end markets like new energy (photovoltaic backsheets, lithium batteries) and electronic-grade high-purity titanium dioxide. This forms a complete “resource-technology-application” industry chain. With stricter environmental policies and growing high-end demand, the industry chain integration is accelerating, with leading enterprises enhancing their international competitiveness through vertical resource layout and horizontal technological collaboration.

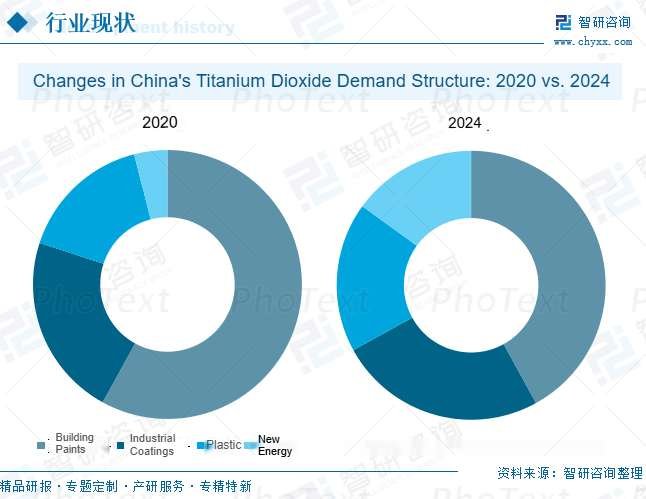

China’s titanium dioxide downstream demand structure is undergoing significant changes. The coatings industry remains the largest application field, but due to adjustments in the real estate sector, the demand growth for architectural coatings has slowed, and its market share has significantly declined. Meanwhile, the demand in the new energy sector (photovoltaic backsheets, lithium battery materials) is rapidly rising, with its share increasing from less than 5% to around 15%. Among these, the photovoltaic sector is growing at an annual rate of 27%, and 15 tons of titanium dioxide are required for each 1GWh of power batteries. The plastics industry maintains a stable share of 18-20%, but demand for chloride-process products in high-end engineering plastics has increased. Additionally, the application of electronic-grade high-purity titanium dioxide (purity ≥99.999%) in emerging fields such as semiconductor packaging is expanding rapidly, driving the demand structure toward high-end products. Overall, demand is transitioning from a real estate-driven single model to a diversified structure of “new energy + high-end manufacturing.”

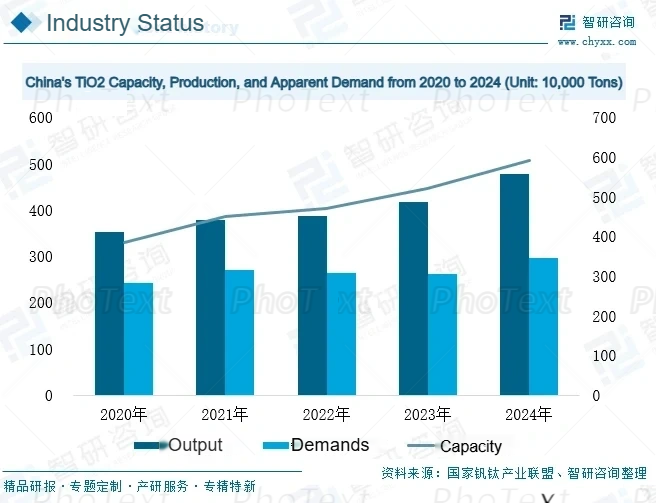

China’s titanium dioxide industry is currently undergoing a deep adjustment in its supply-demand structure, with its market dynamics closely intertwined with the real estate cycle. As a core downstream sector, fluctuations in the real estate market directly reshape the industry’s supply and demand pattern. In recent years, due to pressures on new home sales and a slowdown in development investment growth, the demand for titanium dioxide has significantly decelerated. At the same time, industry capacity continues to expand, with production reaching 4.766 million tons in 2024, while apparent demand is only 2.956 million tons. The supply-demand gap has widened to 1.81 million tons, putting downward pressure on capacity utilization. Although policy incentives, such as urban village redevelopment and urban renewal, have released some incremental demand, the pace of capacity expansion and demand recovery is mismatched in timing. Additionally, the export market faces trade barriers such as the EU carbon tariff and anti-dumping measures from India. The industry’s overcapacity issue is unlikely to ease in the short term, and the market will continue to experience a “high capacity, low load, weak profitability” imbalance.

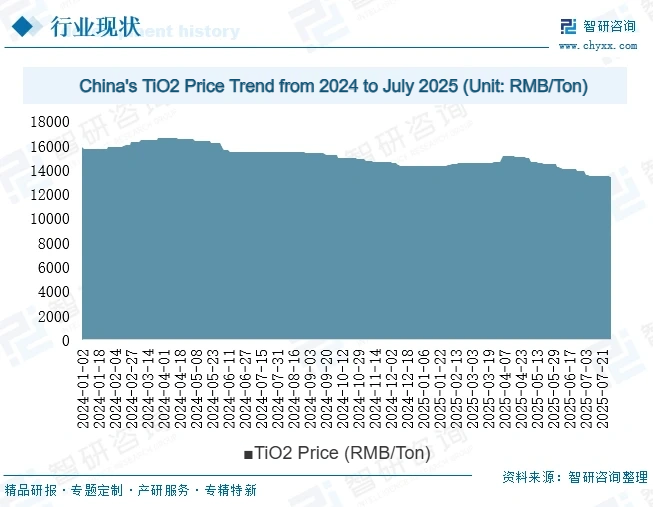

Since 2024, the market price of titanium dioxide in China has shown an overall downward trend. At the beginning of the year, the domestic average price of titanium dioxide was 16,483.33 RMB/ton, and by the end of the year, the average price had dropped to 14,900 RMB/ton, reflecting a decrease of 9.61% throughout the year. The implementation of the EU anti-dumping tariff has exacerbated the overcapacity issue in China, leading to a decline in titanium dioxide prices and increasing operational pressures on enterprises. However, the supply of raw material titanium concentrate remains tight, with prices running at high levels, providing strong support for titanium dioxide production costs.

Since 2025, the overall demand for titanium dioxide has been weak due to increased trade policy uncertainties, compounded by the deep adjustment in the real estate sector. From January to July, market prices experienced a “rise and fall” trend. In the first quarter (January to March), prices increased by about 600 RMB/ton due to the price rise of titanium sulfate and tight supply caused by seasonal maintenance during the Chinese New Year, but the growth was suppressed by demand depletion and increased export tariffs. In the second quarter (April to June), weak demand led to a rise in enterprise inventories, and prices continuously declined. In May, a price reduction of 500 RMB/ton by leading companies triggered a chain reaction, and in June, during the off-season, major companies further lowered prices by 1,400 RMB/ton, narrowing the price difference between sulfate-process and chloride-process products. Many companies were nearing their cost line or even operating at a loss, with nearly 20 companies halting or reducing production. In July, the market remained sluggish, with strong wait-and-see sentiment from downstream sectors, and prices continued to trend lower.

In recent years, with the continuous strengthening of environmental protection policies and the rising demand for industrial upgrades, chloride-process titanium dioxide has become the core direction of the industry’s green transformation due to its advantages in low energy consumption and minimal pollution. This process requires strict raw material purity (greater than 99.5%) and precise control of reaction temperatures (1200-1400°C), creating a globally concentrated technological barrier. Only international giants such as Chemours, Tronox, and a few domestic companies like Jinzhou Titanium Industry hold core patents.

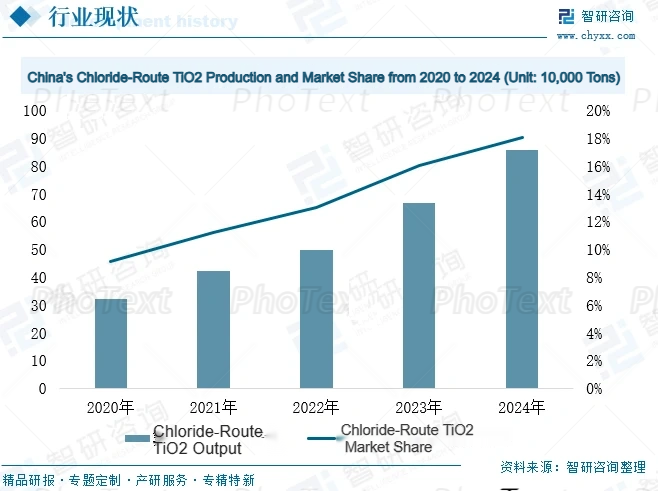

Notably, China has successfully broken through key technologies in fluidized bed chloride and molten salt chloride through collaboration between industry, academia, and research, achieving domestic substitution for high-end electronic-grade titanium dioxide (purity ≥99.999%). As of 2024, the total capacity of fluidized bed chloride technology has surpassed 1 million tons, with production increasing from 321,000 tons in 2020 to 858,000 tons, achieving a compound annual growth rate of 27.86%. This has driven the market penetration rate from 9% in 2020 to 18% in 2024, and it is expected to exceed 20% in 2025. This marks China’s accelerated transition from a major titanium dioxide producer to a technological powerhouse.

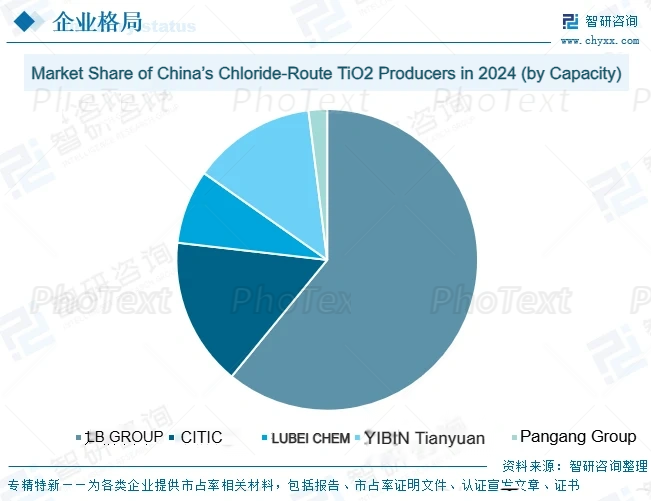

China’s chloride-process titanium dioxide industry has formed a “one leader, many strong competitors” competitive landscape, with leading enterprises holding significant advantages, but emerging players are rising. According to the Titanium Dioxide Industry Technology Innovation Strategic Alliance, among the 42 national full-process producers in 2024, only 5 have chloride-process production capabilities. Among them, LB Group is the leader with 460,000 tons of chloride-process capacity, accounting for 61% of the national market share. Its total capacity of 1.51 million tons (including sulfate-process production) makes it the third-largest titanium dioxide producer globally.

CITIC Titanium, as a representative of pure chloride-process enterprises, ranks second by leveraging the advantages of the Jinzhou industrial cluster. CITIC Titanium plans to start a 320,000-ton chloride-process titanium dioxide project in 2025, significantly increasing its market share. Panzhihua Steel has made breakthroughs in high-end products with a 60,000-ton molten salt chloride production line, filling the domestic technological gap.

Driven by environmental protection policies and new energy demand, the environmental and quality advantages of chloride-process technology will accelerate the industry’s concentration, and technological breakthroughs and raw material self-sufficiency will become key competitive factors.

China’s chloride-process titanium dioxide industry is expected to follow three major development trends: high-end, green, and global. With the continuous strengthening of environmental policies and the advancement of the “dual carbon” goals, chloride-process technology will accelerate the replacement of the sulfate process, and its capacity share is projected to exceed 60% by 2030. The industry will shift toward high-value-added sectors such as new energy (photovoltaics, lithium batteries), high-end coatings (automotive, marine), and electronic-grade products (semiconductors), promoting an upgrade of the product structure. At the same time, leading companies will build overseas facilities (e.g., in Southeast Asia) to bypass trade barriers, and leverage full-industry-chain layouts and technological innovation to enhance international competitiveness. Industry concentration will further increase, forming a “strong-get-stronger” competitive landscape.

Specific development trends are as follows:

- Accelerated Replacement of Sulfate Process by Chloride Process

Over the next 5–10 years, China’s chloride-process titanium dioxide industry will enter a rapid expansion phase. With tightening environmental regulations (sulfate process listed as restricted), chloride-process capacity will continue to rise, expected to exceed 60% by 2030. New capacity will mainly come from leading companies such as LB Group (460,000 tons of chloride-process capacity) and CITIC Titanium (320,000 tons under construction). Meanwhile, Pangang Group’s 60,000-ton molten salt chloride line has achieved stable operation, validating the feasibility of domestic technology. Furthermore, the low carbon emissions of the chloride process (1.8 tons CO₂ per ton) align with the “dual carbon” targets, driving the industry toward green transformation. - Growth in High-End and Functional Product Demand

Demand for traditional architectural coatings has contracted due to the real estate downturn. However, new energy (photovoltaics, lithium batteries), high-end industrial coatings (automotive, marine), and electronic-grade titanium dioxide (semiconductors, MLCC) will become core growth drivers. Demand for photovoltaic backsheets is increasing at 27% per year, and 15 tons of titanium dioxide are required per 1GWh of lithium batteries. By 2030, the new energy sector’s demand share is expected to rise from 15% in 2025 to 25%. Meanwhile, breakthroughs in domestic high-end chloride-process products (e.g., CR-350 coating grade, CR-340 plastic grade) and electronic-grade high-purity titanium dioxide (purity ≥99.999%) will further enhance the competitiveness of Chinese enterprises in the international market. - Global Expansion and Industry Integration

In response to trade barriers such as EU anti-dumping duties, Chinese companies are accelerating overseas facility construction (e.g., LB Indonesia project) to expand into emerging markets in Southeast Asia and Africa. With industry consolidation and technological iteration, production lines with capacities exceeding one million tons will become mainstream, and industry concentration is expected to rise further. Leading companies such as LB Group and CITIC Titanium will strengthen competitive advantages through full-industry-chain integration (e.g., “titanium ore–titanium dioxide–new energy materials” closed loop), while small and medium-sized enterprises gradually exit the market due to technical and environmental barriers. In the future, companies with overseas capacity layouts and high-end product R&D capabilities will occupy dominant positions in global competition.

[/pwprotect]

Some parts of this post are password-protected. You can obtain the password through either of the following methods:

- Request it via email at info@etio2.com.

- Join the LinkedIn group “TIO2 WORLD – Titanium Dioxide” for ACCESS CODE.